Crypto - Quo Vadis

The crypto economy needs more than being left alone by over-reaching regulators.

Crypto markets showed some signs of life over the last couple of months. Most of that is driven by relief from operation choke point 2.0. - an authoritarian attempt by the US political establishment to strangle a nascent industry by cutting it off from the financial system and by bullying its key actors. The hopes are high for everything to change under president Trump. To flourish, the crypto economy needs more than neutral regulators. This post explores some of the down-stream factors that might make crypto great again.

Status Quo

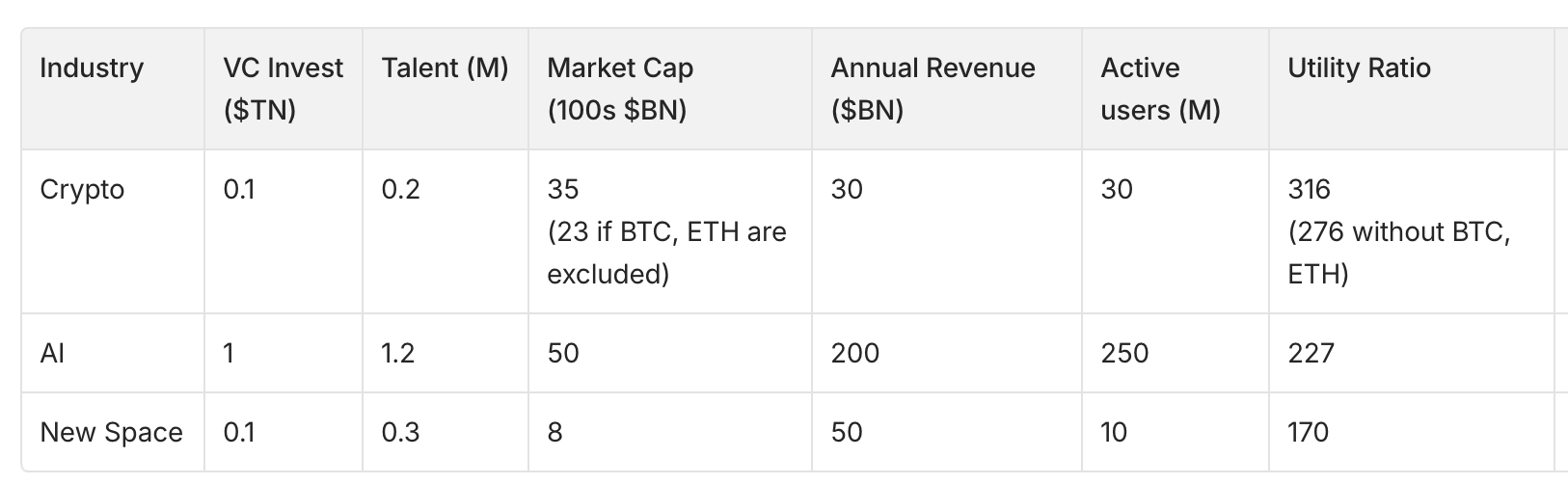

Where are we as an industry? A lot has been written about the state of crypto to provide a bottom up view of what's going on in the industry in terms of adoption, developer momentum, regulation, use cases etc. But how does progress look like relative to other emerging industries? To get a sense for an industry's progress we could think of its inputs and outputs:

Total value generated could be defined as a mix of quantitative metrics: market cap + annual revenue + active users for example.

Resource input could be defined as a mix of metrics such as venture capital injections and talent working in the industry.

The higher the ratio, the more resource efficient is the industry. For simplicity I expressed the market cap numbers in 100x $BN instead of trillions to give them reasonable weight relative to revenues and users. The utility ratio was derived by calculating (Market Cap + Annual Rev + Active Users)/(VC invest + talent).

This is an extremely over-simplified way of benchmarking progress across industries as it leaves aside any qualitative elements and treats all inputs equal. The utility of a technology is something very subjective though as we've seen when the debates of Bitcoin's usefulness relative to its energy demand unfolded - something we see with AI again now but somehow with much less emotion at play. Hence, I stuck to simple quantitative measures and equal weights.

Caveat #1: prices might sharply correct downwards anytime and volatility is higher than in other sectors

Caveat #2: A lot of the market cap value is derived through BTCs and ETH's monetary premium that is fundamentally different from market caps derived from profit generating companies

Caveat #3: all numbers are averages from the various spectra of data available [1]; crypto monthly active user numbers quoted from a16z’s crypto report seem high

Caveat #4: there is a time lag between resource injections (capital, talent) and value generation expressed in market caps, revenues and users. Resources put to work at t0 might yield outcomes many years into the future.

Despite all those flaws it seems that the crypto economy at least in tendency does pretty well in terms of utility value if benchmarked against other nascent tech industries. This goes against public sentiment. Still, there is huge potential for growth if the industry gets the following things right.

Regulation

The end of operation choke point 2.0 is great but it can only be a starting point. So much injustice has been done to the crypto economy that it leaves the effectiveness of western constitutions and court systems in doubt. From the OFAC sanctions against Tornado Cash's smart contracts as 'property' (which got successfully appealed) to the European Commission's attempt to undermine online privacy in the name of child protection all the way to countless, baseless subpoenas against many major actors in the space leading to no tangible outcomes. We live in a time where the rule of law is increasingly captured by political interests. This trend will be amplified by a climate of populism as most citizens in the west would rather like to see their particular interests being represented as opposed to benefiting from a maximally neutral and predictable system of law rooted in western constitutions.

The two enemies of the people are criminals and government, so let us tie the second down with the chains of the Constitution so the second will not become the legalized version of the first.

Thomas Jefferson

That said, it is refreshing to see governments change their minds on critical policy topics from time to time. We’ve seen Trump and many other Bitcoin sceptics turn around after a while. Be it because of new insights or shifting incentives. It seems that many officials have been perceiving Bitcoin as a threat to the US dollars dominance before they realised that Bitcoin doesn’t compete with fiat money but with wealth preserving assets like gold, real estate, art etc. Their fear of losing control over a weaponised financial system might be more rooted in reality but they started seeing the benefits of neutral, open architectures that can still be sufficiently controlled at the interface level, entry and exit points. Therefore, we expect crypto regulations to soften in the west over the next few years.

Zooming out a bit, it seems that the west is slowly forming a consensus around the fact that bureaucracy is killing productivity. And productivity is in high demand in a de-globalising world. This is a development we’d classify as an inflection - a profound shift in politics unleashing novel behaviours at scale. Imagination for what is to come might be drawn from Thatcherism or Argentina’s Milei pioneering radical government reform with early successes surprising to most. Trump might follow suite in the US while Europe is busy picking up the pieces after the collapse of two of its leading governments in Germany and France. At Inflection we perceive crisis as opportunity and are optimistic that Europe will get its act together like it always did over hundreds of years of wars and revolutions.

We expect over-regulated industries such as finance and technology in general to benefit from such developments, including the crypto economy. Reforming Western democracies by cutting through red tape and reducing spending may be painful in the short term but holds vast potential in the long term.

Incentives

This brings us to incentives. The crypto sphere is great at quoting Charlie Munger with his famous words:

Show me the incentives and I will show you the outcome.

In tendency, the industry is leaning towards early liquidity through token launches. Arguments underpinning that school of thought are manifold: (1) early liquidity allows retail investors to participate in a network's upside much earlier than in public stock markets. Crypto is more egalitarian and fair than most other industries. (2) Fast liquidity incentivises money and talent to flow towards the best ideas more efficiently. (3) Projects “owned” and controlled by the community of users should be more aligned with the public’s interest. etc.

In principle I agree with those ideas. Yet, the devil is in the details. As long as private markets exist in crypto we will see founders and early backers enriching themselves on the back of retail investors. Through many cycles we've seen the same play book unfold across ICOs, NFTs all the way to meme coins, just that the actors have changed and the mechanics are iterated on. A group of people is hacking together a product, launches a token, sells vast amounts thanks to short or no vesting before the project is de facto abandoned. This behaviour is zero sum. It slows down progress, caused a lot of the regulatory fall out and public trust issues.

As a venture firm we think in decades and act in years but that is not true for many of our peers. Crypto VCs and their short term acting capital bases are fundamentally at odds with long term progress. More than a few times we have seen investors putting pressure on founders to launch a token as fast as possible - ignoring the long term effects on the organisation and its stakeholders. Market structure and a lack of large acquisitions or IPOs amplified such behaviour. We have to do better than this.

We encourage innovators to revisit best practices in private venture markets. There is a reason for founder shares re-vesting from financing round to financing round. There is a reason for tag-along and drag-along clauses. There is a reason for liquidation preferences and waterfalls. There is a reason to limit secondary sales for early investors and founders to certain amounts and pricing them based on private market valuations. That reason is long term stakeholder alignment to build meaningful things instead of the financial hedonism we often see in crypto.

Infrastructure

Crypto infrastructure improved massively over the last 4 years and is likely to continue to do so. E.g.,

Transaction Costs: L2 transaction costs reduced by 90%+ relative to main chain

Data storage: EIP-4844 (proto-danksharding) optimised data storage of additional 2MB per block

Interoperability: enhancements through cross chain bridges

UX: account abstraction, embedded wallets, smart accounts

It seems that block space overall is much less of an issue going forward and that UX is improving slowly and steadily. Yet, all of this is still emerging and there are more challenges ahead that are less solved for the time being, e.g.,

Privacy enhancements through ZKP, TEE and FHE implementations

Decentralisation of block building to maintain sovereignty

Deep integration of crypto rails into traditional financial infrastructure (or the other way around)

Security guardrails and UX for regular users

…

Fundamentally, the industry's infrastructure improved by an order of magnitude relative to 4 years ago. It still isn't perfect for all imaginable use cases but each cost reduction and infra improvement unlocks economic feasibility of new use cases.

Talent

We have seen a net outflow of talent in the industry since late 2021. what is perfectly in line with Chris Dixon's price-innovation cycle. The core idea being that rising prices create interest and awareness what leads to new ideas and ultimately talent and new companies in the space. What kept new talent from joining was negative public sentiment coupled with the fear of being punished by regulators but this bottle neck is overcome now.

Not just the quantity but also the quality of talent joining the industry will be foundational for future progress. In past cycles we've mainly seen young, curious risk takers joining an infancy stage industry. This is very different today with trillions of dollars in market cap and a broad based institutionalisation of the industry. At Inflection our hope is to see more talent with inter-disciplinary backgrounds join. People who have seen and created greatness in other technology industries to break open current misconceptions and group think in crypto.

Ideas

Closely related to talent are ideas. They are co-dependent in fact. When the crypto economy took off its actors aligned in many powerful visions of creating state free money for the world, a permission-less and open world computer, a decentralised web, an eternal library, open source Wall Street and markets as a mechanism to predict the future. When I joined the industry a decade ago those ideas felt far more powerful than anything else people have been working on - e-commerce, enterprise SaaS, dating or payment apps for example.

These days most teams seem to work on incremental improvements (faster, cheaper, better UX) instead of unlocking fundamentally new behaviours. This was driven by a lack of infrastructure readiness as well as a maturing and institutionalising industry with less radical, less interesting ideas. Fixing MEV, bringing down transaction costs, tokenising existing assets, stable coins, AI powered meme coins feel very different from earlier ambitions.

Further, the world changed as we accelerated in the exponential age. Opportunity costs to join the crypto economy exploded from an impact perspective. As a young, renegade genius would you like to contribute to a new financial system or populate Mars, defend western civilisation, make energy / compute / knowledge abundant or engineer life? Through the convergence of emerging technologies and break neck pace increases in AI capabilities the opportunity costs to join crypto for its diluting causes seem higher than ever.

That said, at Inflection we believe that crypto technologies are a huge enabler of various new behaviours and that they will play a key role in defending democratic civilisations and contribute to the agent economy by providing economic rails and attestation services to distinguish between humans and machines besides many other things.

All of the above ingredients make the recipe for building meaningful tools for humanity. It will lead to the formation of new companies and the launch of ground breaking products very few can dream up today. To explore them collaboratively is what excites us at Inflection.

[1] Resources:

Nearly 190k people work in crypto, more than 50% located in the west

New data shows rapidly expanding space workforce

54 New Artificial Intelligence Statistics (Dec 2024)