Depth vs. breadth

Maybe investors should use both System 1 and 2 thinking?

There is a great number of points in every person’s life when a line of subjective inquiry ends with the thought “I don’t know enough about this to go one level deeper.” And if you have an inquisitive 4 year-old then it happens multiple times a day. Tonight’s example:

Why won’t you fall out of a rollercoaster?

Well, you are usually strapped in.And why not, more reasons?

I guess if you’re going really fast in a loop then you’re pressed against the seat anyway by the centripetal force and won’t fall down.But how can it hold you?

Hm, the seats are really durable and they are held by really strong metal bars that also support the wagon.Is it harder than teeth?

Uhhh, I think so? In some ways…And what about dinosaur teeth?

Good question…

Because of the nature of our work, I’m usually on the kid’s side of this dialogue with founders or researchers. (Hopefully with slightly less non sequiturs involving dinosaur teeth.) We try to understand the tech as quickly as possible, have good conversations about the business at hand, follow our own curiosity and the specific complexities of the area. Ideally, we have a prepared mind and can skip the first couple of layers of questions and dive into the more interesting stuff faster. In some cases we’ve written about the topic publicly before, or we’re close to companies who have indicated where the interesting problems of that space exist. But there comes a time when the response amounts to “Good question…” in some more or less strategically phrased way.

Why does the depth matter?

(now it’s nested list time, get ready)

We care about how deep we can go because it shows us something about the founder's way of thinking. To give some examples, it shows us:

a. How much the other person thought about their business, which is a proxy for:

i. How obsessed are they?

ii. Are their level of curiosity greater than ours?

iii. Are they stuck in a particular way of thinking or can they change perspectives?

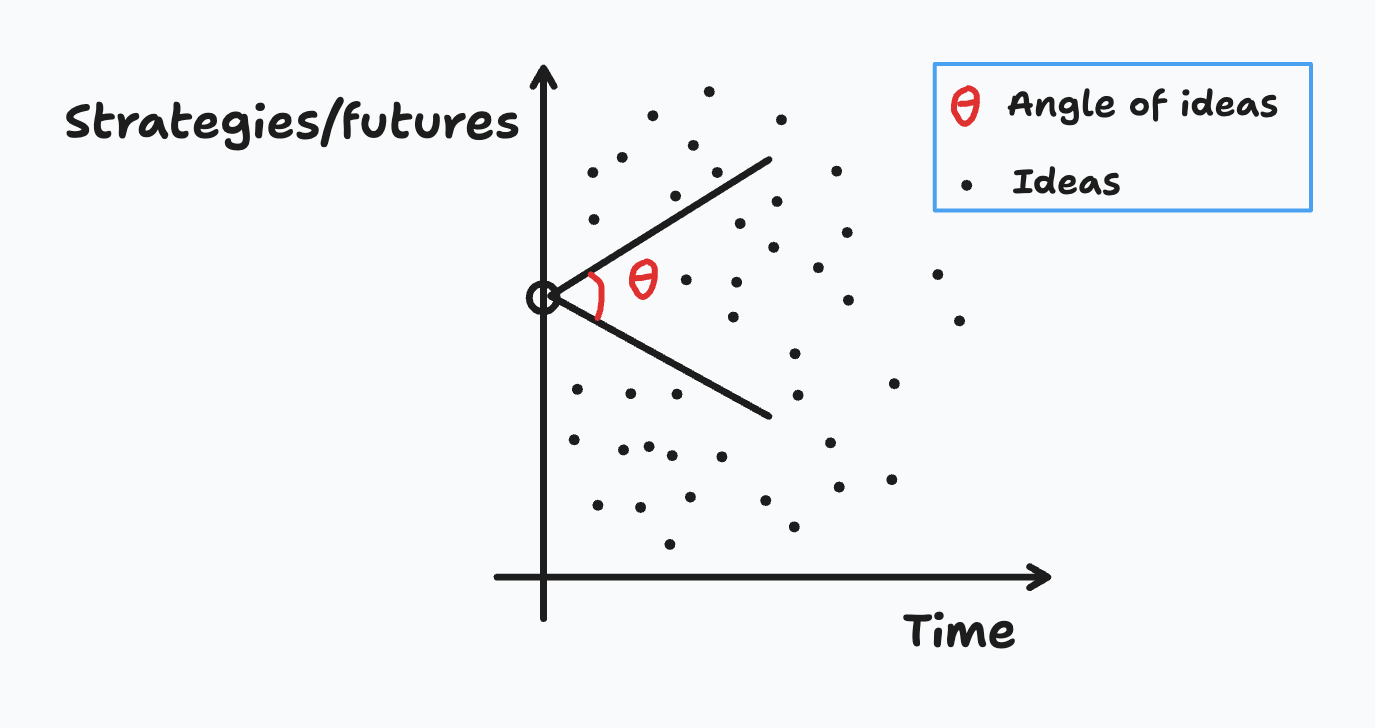

b. What the founder’s angle-of-ideas (see illustration below) for the future of the company looks like, which shows:

i. Priorities and certainty in predictions

ii. What dimensions of the plan are fixed vs. flexible?

iii. Understanding of getting big, ambitious projects done

c. How the person deals with not knowing, this can cause:

i. Avoidance, misdirection, conversational “tactics”

ii. Nervousness and awkward silence (side note: it doesn’t make us uncomfortable)

iii. Making stuff up, acting like you know when you don’t

iv. (this is the worst) Actually thinking they know when they don’t

v. Acceptance of lack of understanding as a common part of going deep into something

Bad reasons and people who use them

The most frustrating situations we face aren’t the ones where the people we talk to simply don’t know and we wouldn’t expect them to know more, or even where people make stuff up (doesn’t happen so often). Many business conversations end up becoming rhetorical battles. Some companies try to fight it systematically (see Bridgewater’s real-time meeting scoring system, and Amazon’s memo practice), but before there’s much of a company we need to go for the individuals shaping the culture. If someone is overusing techniques from “How to make friends and influence people” in early conversations, then we have a hard time believing they’ll hire the right people and instill them with a culture that cares about progress over politics.

The counter argument to this is someone who seems overly sales-y to us, might actually be great sales people in certain settings. Since both hiring and fundraising are sales games, besides selling the product, it might be the right person for that company. But authenticity needs to be present.

My absolute worst pet peeve is the “you don’t need to know that, and so I didn’t look into it”-style response, unless it comes with very good reasoning for why we’re asking the wrong question (it happens, see dinosaur teeth). Arrogance isn’t necessarily bad in a founder; to some degree you need to believe in yourself to an extraordinary amount to start a company; but if it’s paired with hiding insecurities and going on the defensive when faced with some limit of their own knowledge, then that rather shows a lack of open-mindedness and curiosity. The feeling we get is “trust me, bro” and when we don’t trust, the counter is “Oh, so you don’t have conviction”. Or inversely, we hear of other investors committing on very short timelines, and the founders saying “They had very high conviction”. But on what exactly?

Conviction capital

To us, having high conviction doesn’t mean that we think the company has a particularly high probability of success, conviction means that we’ve done the work to understand what we are underwriting, and importantly what we’re not. Conviction is multi-dimensional, at the earliest stages, it’s 80%+ dimensions in the founder traits, but what might not be obvious is that every aspect of the company is a reflection of the founder. The founder is the soil and the company is a flower whose petals and roots we want to observe to understand what brought such a thing to life.

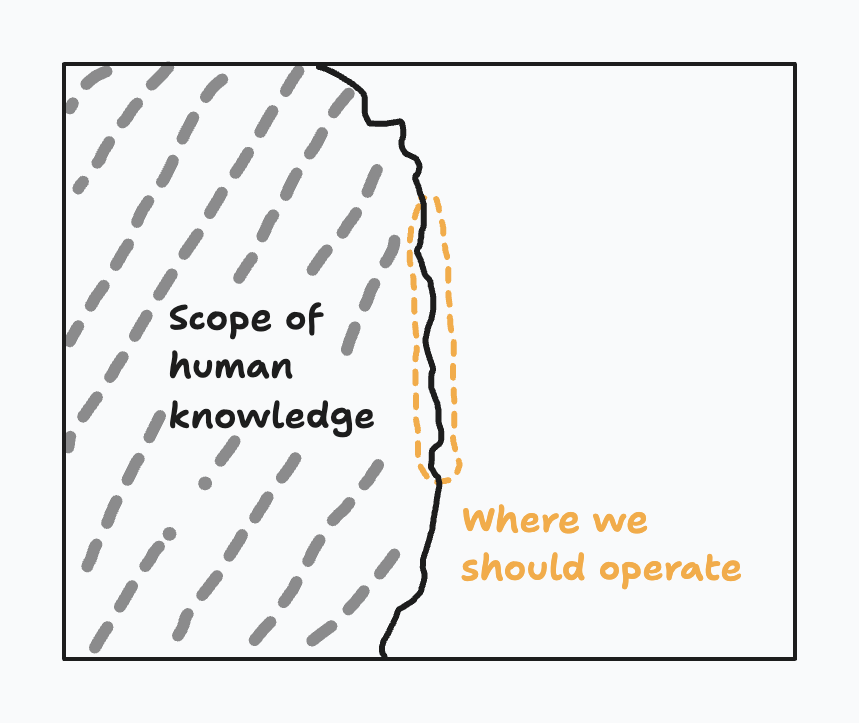

We need to be the truth-seeking biologists and horticulturists, not florists; we need to be Georg Mendel taking careful note of cause and effect rather than a superficial observer. I’m saying this on an individual company-level, as well as a market level. Only by studying something carefully can we know it. This assumes that we believe in something being knowable, of course. The obvious conclusion to seeing investing as a knowledge-enhancing activity is that in order to do great investments, we need to operate on the fringes of what is known. Some things should be more certain, like the physics governing the fundamental technology, or that someone will want to buy it, should it work (aka. “Big if true”). Other things can be more uncertain. What we don’t want, are the companies moving entirely within the scope of human knowledge—the playbook companies (note: my own em dash). We are not interested because those companies will be funded by other pots of money, so our dollars are not really value-adding.

We build conviction around a founder, and their ability to be the best at building exactly that company they want to build. This conviction-building requires us to understand everything around the company possible, up to some level where the uncertainties on the predictions become too vague to have an impact. This includes technology, market dynamics, other players, funding landscape, etc. It also includes personal judgement on the founder as a person, spending time with them, getting to know them over calls, walks, coffees, and awkward silences.

These are all variables in the conviction equation.