Balancer

ETFs and liquidity for the world.

The first wave of financial technology companies brought us robo advisors, neo banks and mobile first insurance companies. All they do is providing their customers with better interfaces, user experience and workflows. They are rather optimising than really innovating as most of them are built on the archaic, siloed and inefficient financial infrastructure of the 20th century. The next generation of fintech companies will look very differently from that. Innovation won't be limited to slick mobile apps and some process optimisations but it will transform the backend of finance. It will enable us to create new, internet native pipelines to let money, assets, value and data flow globally and peer to peer without restrictions. A more recent umbrella term used to describe these types of technologies has been ‘decentralized finance’ (DeFi) or ‘open finance’. Companies and projects innovating in this field will do to banks and financial institutions what the internet did to post offices. Or to bastardise Marc Andreessen’s famous quote:

Software has been eating the world. Now it’s coming for the public sector - starting with money, followed by financial services and ultimately - governance.

What sets Defi apart from conventional fintech?

So what is it that sets innovation in Defi apart from previous waves of financial technologies?

Programmability: DeFi software is openly programmable. Programmatic financial products and applications can be created by everyone with an internet connection and the appropriate skill sets. Gate keeping through proprietary APIs and databases doesn't apply under this new paradigm. The new financial pipelines are rooted in open source software protocols similar to the web's suite of protocols.

Composability: Defi components can be considered as 'money legos'. They can be plugged together in various forms to create new applications and workflows, just like lego blocks can. A network of money legos comes with the qualities of pooled liquidity and interdependent network effects serving as strong bootstrapping mechanisms. But composability comes at the cost of ripple down effects - whenever one component fails it might have negative (if not fatal) consequences for other components that are relying on it.

Sovereignty: current financial infrastructure is organised in closed silo databases under the control of banks and financial institutions. Customers have to rely on their banks to access and move their assets. If the bank is closed or denies access for some reason customers can't do much about it. In DeFi customers are holding the keys to their financial assets themselves (literally). They can access and move around their assets anytime they like as the ledgers these assets are sitting in are running 24/7 and can't be controlled by any group of people. Asset owners alone decide which interface to use when and in which context - not the banks.

Transparency: Each component of Defi software is transparent with regard to the mechanics of the underlying programs moving around assets and data (smart contracts). Insights into the flow of assets between pseudonymous accounts (public key addresses) as well as the structure of nested financial products can be provided continuously. They also can be cryptographically verified by any outside observer at any given time (continuous accounting) what could have prevented the subprime crisis or the recent Wirecard debacle. The temporary downside of transparency is a lack of privacy and thereby security. Solutions to obfuscate accounts and the flow of assets at least to a certain level are under heavy development leveraging sophisticated cryptography.

Censorship resistance: Everyone with an internet connection is empowered to create and use financial applications without being limited by any institution or government. Combined with the merits of transparency this renders manual, institutional regulation obsolete to the degree that the software is replacing it - ‘code is law’.

Based on these properties Balancer Labs created the balancer protocol which we believe has the potential to fundamentally transform the financial services industry. Hence, we backed Fernando, Mike, Nikolai and their exceptional team with Inflection as part of their seed round alongside Placeholder, Accomplice and Coinfund.

Programmatic ETFs and liquidity for everyone

Balancer was born out of an idea proposed in 2016 by Vitalik Buterin. In its first iteration Balancer allows everyone to provide liquidity for digital assets for a self set fee. It's like creating a programmatic ETF which rebalances positions automatically whenever prices of the underlying assets fluctuate relative to the remaining assets in the ETF pool. Balancer puts the usual model of asset managers being paid to rebalance positions on its head. Liquidity providers (LPs) holding assets in balancer pools allow traders to swap the underlying assets anytime.

Example: a balancer pool holds say 20% Tesla stocks, 20% Square stocks, 20% Bitcoin, 20% ETH and 20% gold. Now TSLA prices are rising while gold is falling while all other positions are stable. The balancer pool would sell off TSLA and buy gold until the initial weights of 20% each are re-established. The ratio of 20% each stays constant.

This way, traders don't need to wait for another order matching theirs in a clunky orderbook interface. Slippage is minimised through smart order routing algorithms drawing liquidity from multiple pools at once in such way that prices are optimised for the trader.

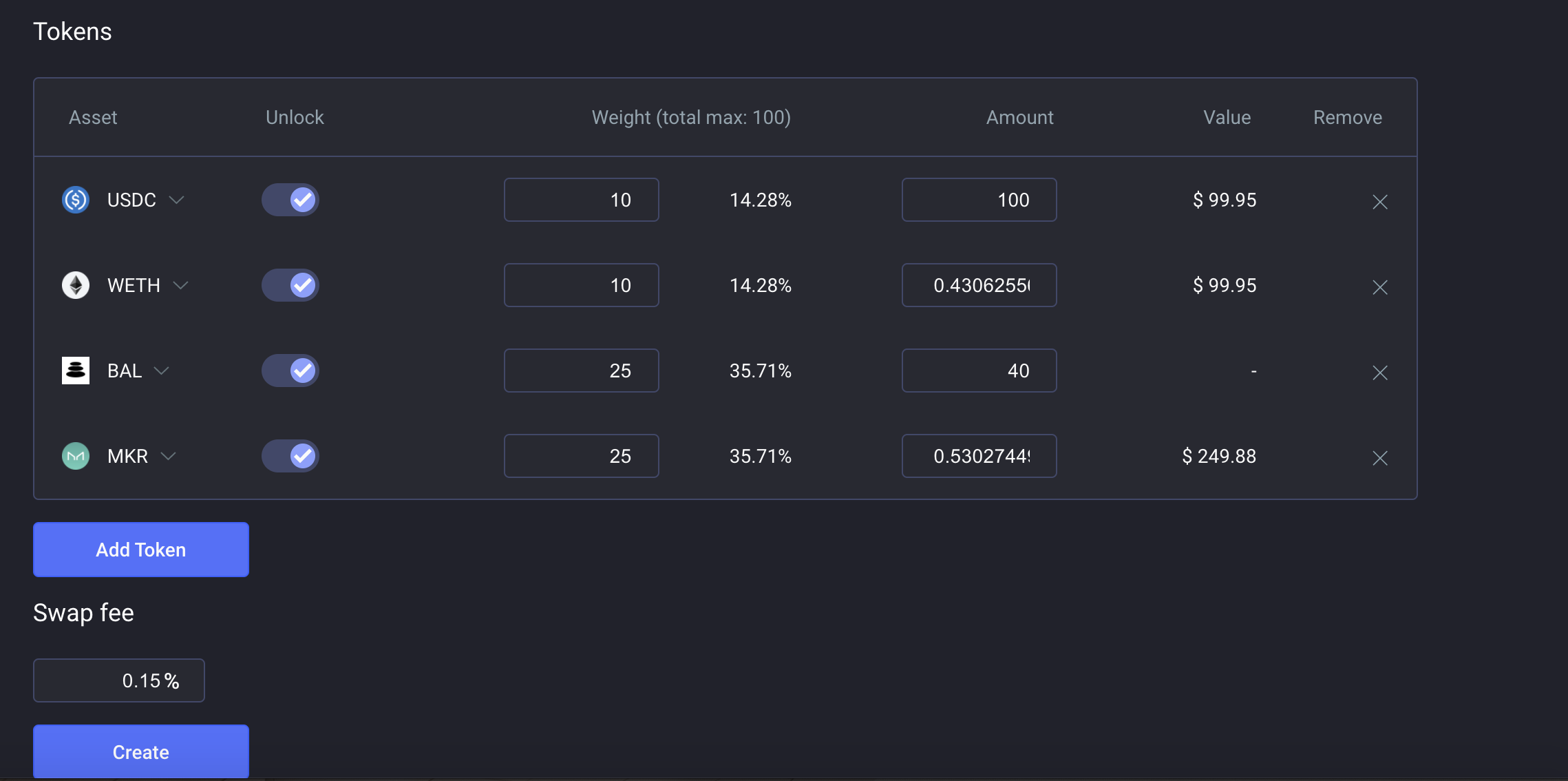

LP view 1

LP view 2

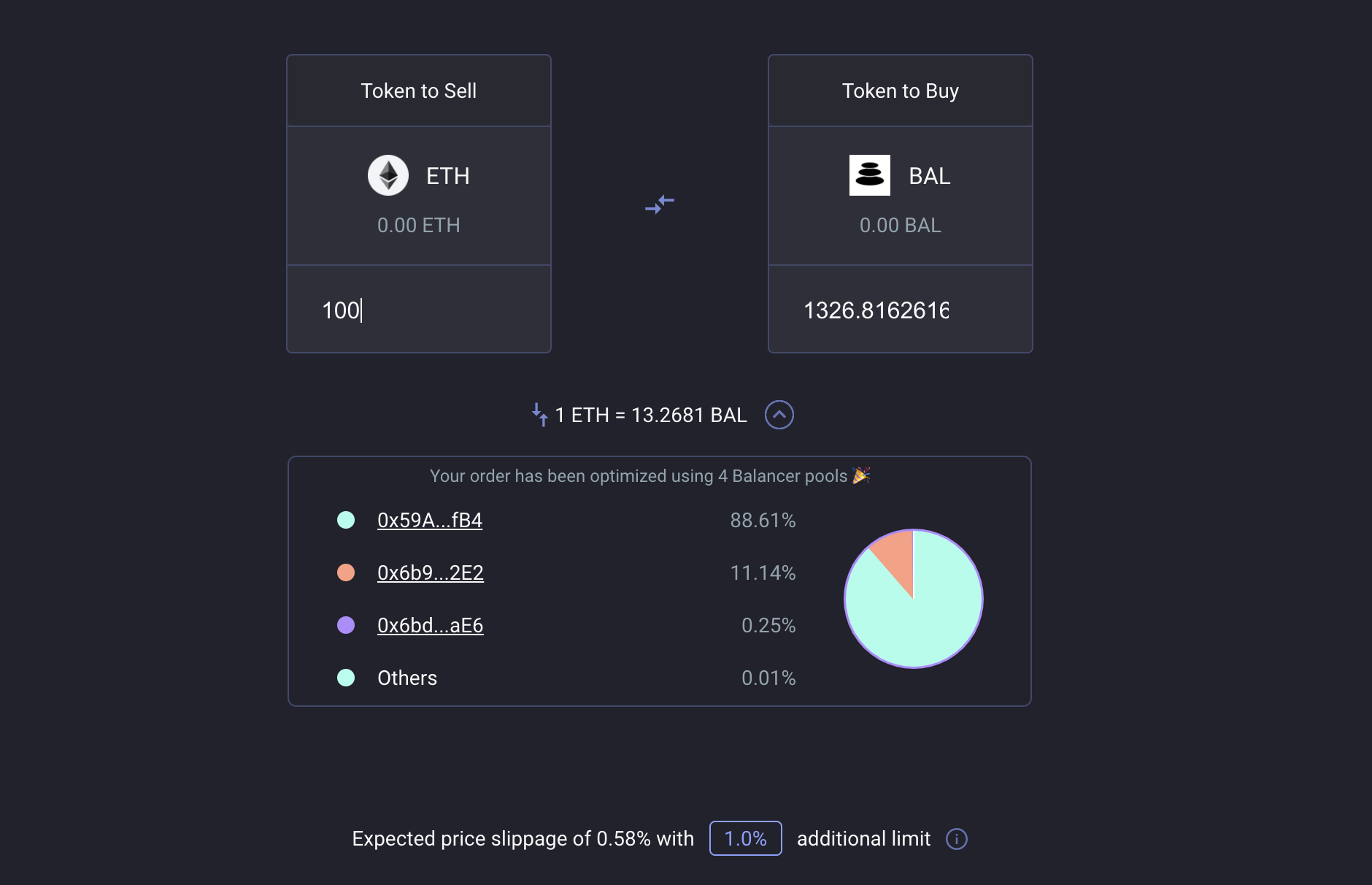

Trader view

Currently the balancer system supports selective crypto assets to be held in its pools - governed by the community. Going forward additional assets will be added including commodities, FX or stocks for example. Balancer's programmability empowers financial architects to create completely new breeds of programmatic index funds and financial products. Trading fees and weights could be defined algorithmically, e.g. taking into account external data feeds like sentiment, momentum, satellite or whether data. Early use cases include programmatic swing trading, interest bearing stable coin pools or liquidity bootstrapping pools.

Shared balancer pools are publicly visible thereby empowering users to mirror the portfolios of the best performing financial architects at zero costs. Liquidity can be added or withdrawn at any point in time, 24/7. Following star investors and mirroring their portfolios becomes as easy as following your favourite band on Spotify.

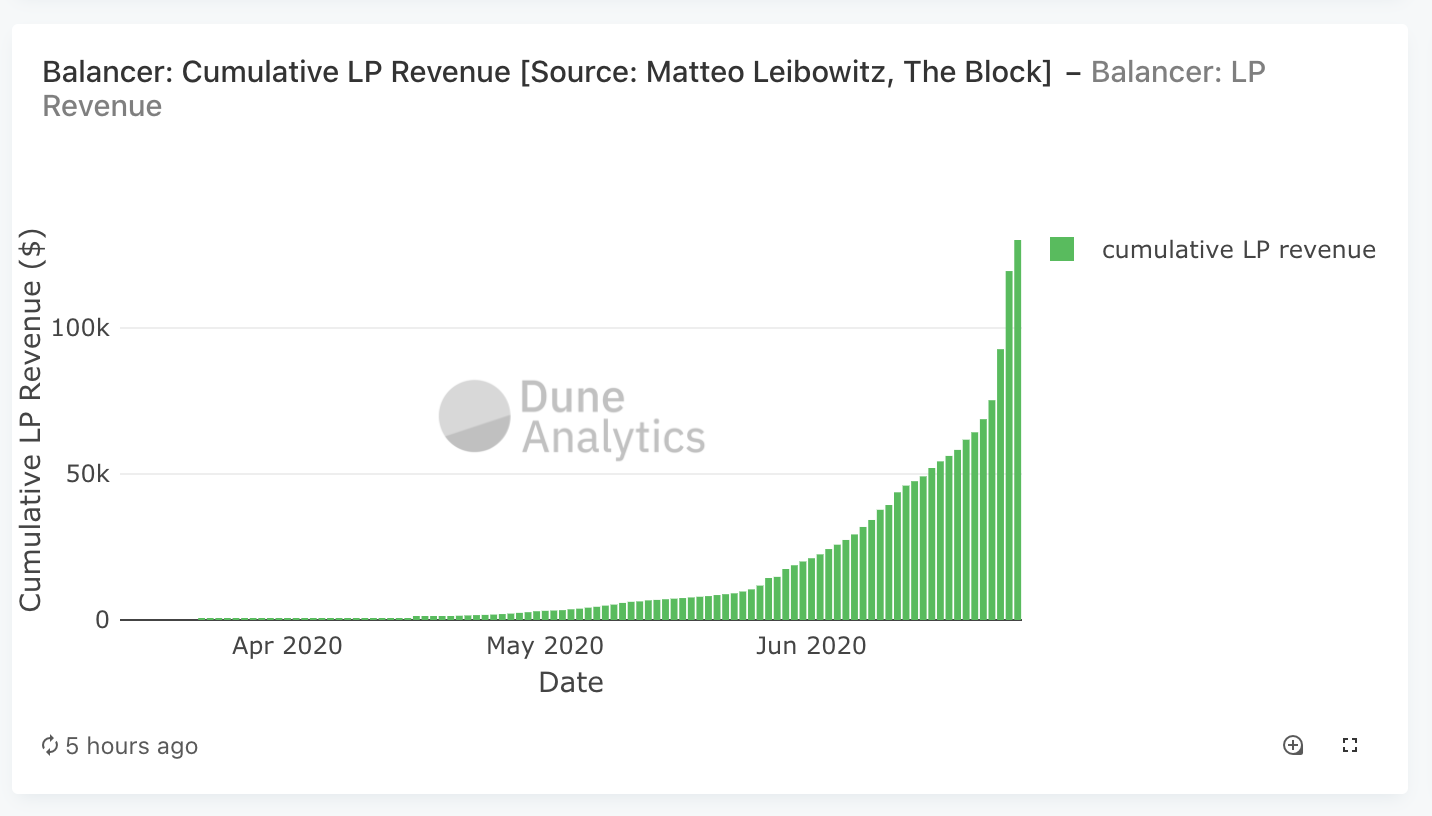

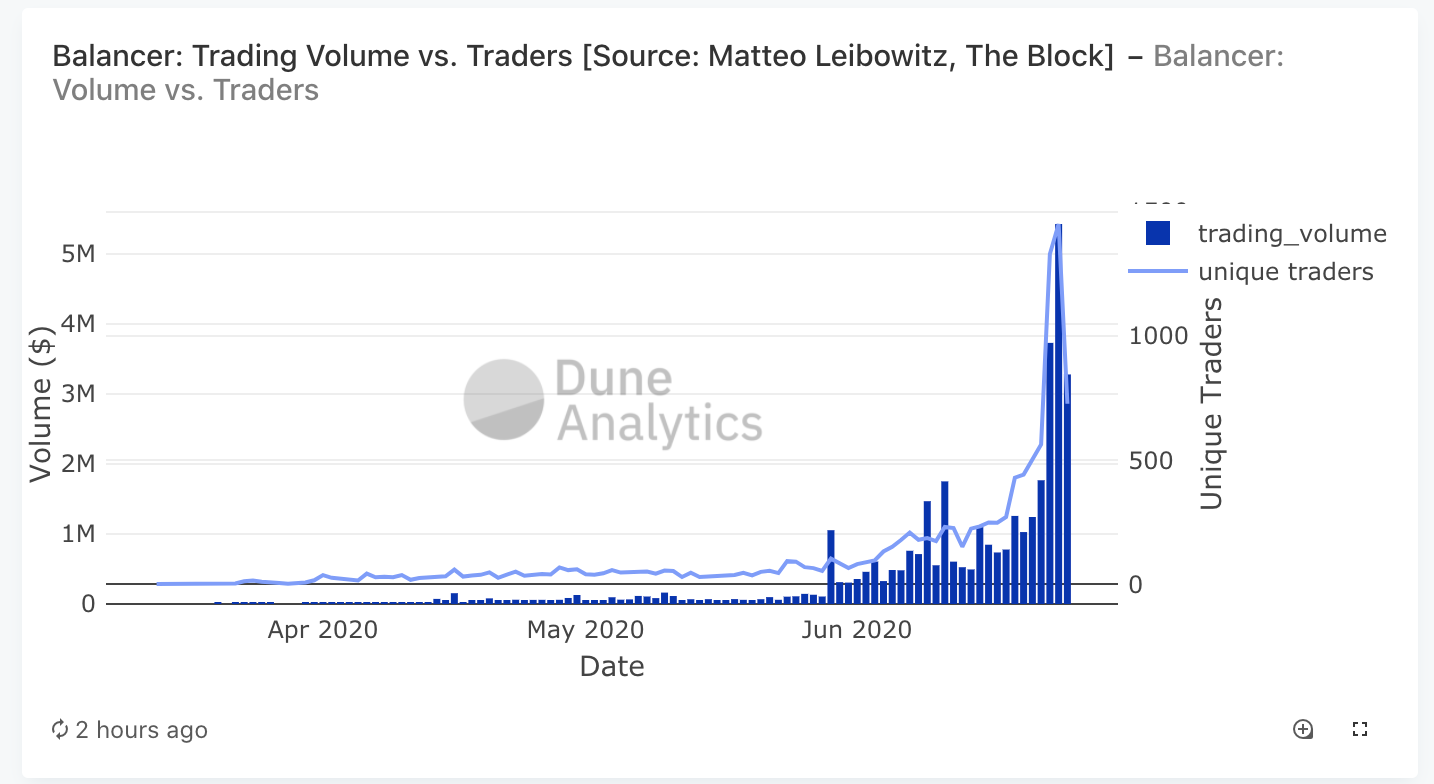

Even though we're early in Balancer's life cycle its fundamentals indicate explosive growth. As of writing >500 balancer pools have been created providing cumulative liquidity of >$71M and a >$35M aggregated trading volume.

Balancer’s growth is fuelled by innovative incentive mechanisms. LPs are not just incentivised by their self set trading fees but also by exposure to balancer's native governance token BAL which is distributed programmatically to them following a transparent supply scheme (liquidity mining). BAL holders are entitled to execute governance rights in order to determine the key parameters of the platform going forward as well as exposure to a protocol trading fee that will be subject to said governance mechanisms.

Onwards & upwards.